This evidence base provides a definition for advanced manufacturing, examines the economic context for advanced manufacturing in the North East, and explores trends in the sector. It also looks at the contribution of advanced manufacturing towards emerging policy areas and the existing regional asset base.

...and 7% of SMEs in the North East LEP area are based in advanced manufacturing

Key sectors

The North East has clear strengths in automotive, pharmaceutical and offshore energy manufacturing

67k

Employees

67,000 people are employed in advanced manufacturing across the region, in over 3,975 businesses

Levelling-up

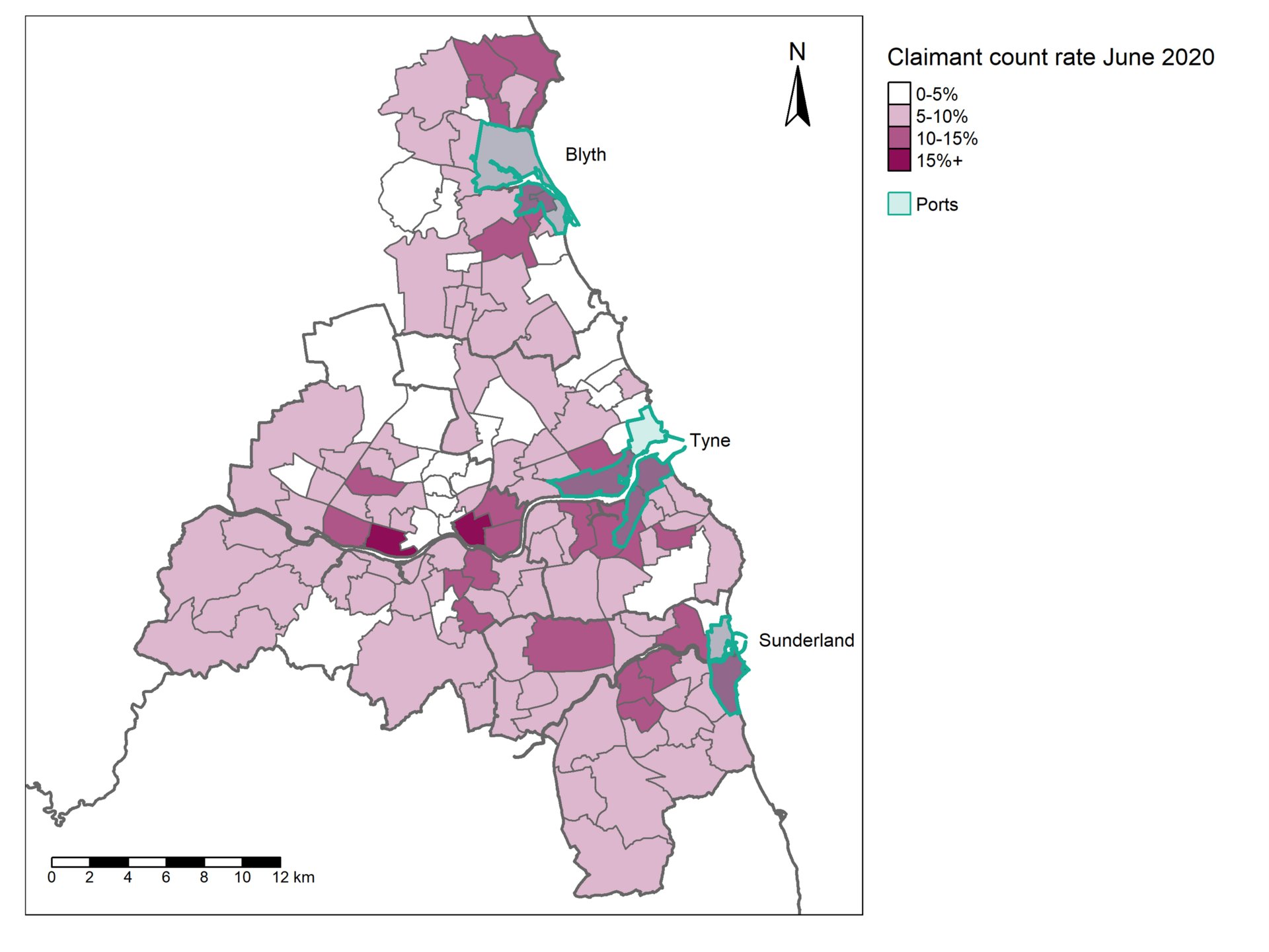

Opportunities in advanced manufacturing are located in some of the more deprived areas in the North East

{{element.textContent}}

Page Menu

{{element.textContent}}

Introduction

Evidence suggests that advanced manufacturing in the North East has strong potential for growth due to our regional assets and capabilities, which is why it is identified as an area of strategic importance in our North East Strategic Economic Plan.

We have developed an evidence base that looks in detail at the region's advanced manufacturing sector, using a range of public and subscription data sources and by reviewing relevant literature.

It provides a snapshot of the current position of advanced manufacturing in the North East LEP area and opportunities for further growth in the region. The evidence base was produced over 2022 and is up to date at January 2023. It will be updated again on an annual basis.

Defining advanced manufacturing

Advanced manufacturing can be defined in many ways, but typically is regarded as manufacturing that is capital and knowledge intensive, uses a high level of technology, includes elements of service provision, and relies on specialist skills[1]. Advanced manufacturing is often linked to the emergence of ‘industry 4.0’, a shorthand for how increased connectivity, analytics and automation can be used to accelerate the manufacturing processes[2]. For instance, advanced manufacturers often use more embedded technologies and techniques such as statistical methods to improve quality, and therefore typically have higher digital readiness levels[3]. This allows advanced manufacturers to continuously improve their production process.

In 2014 the North East LEP’s Strategic Economic Plan identified advanced manufacturing as one of four areas of strategic importance for the North East’s economy, with existing regional specialisms in automotive and medicine manufacturing[4]. The plan also identified the importance of the region’s engineering, research and innovation capabilities which provide underpinning assets for the growth of advanced manufacturing in other sectors such as energy technologies and chemistry.

^Renewing industrial regions? Advanced manufacturing and industrial policy in Britain (2021)

^Industry 4.0: Reimagining manufacturing operations after COVID-19 (2020)

The recent history of manufacturing in the North East

The North East has a long and distinguished manufacturing history, benefiting from a geography providing easy access to the sea through the region’s rivers and plentiful land suitable for the construction of factories and other infrastructure. This history has been punctuated by significant periods disruption and change, but since the 1980s the region has developed clear specialisms in automotive, pharmaceutical, and offshore energy manufacturing.

The opening of the Nissan manufacturing plant on the former RAF Usworth Aerodrome was a key turning point in the development of a North East automotive cluster. This significant investment against a background of declining employment in manufacturing established the North East as an exporter of automotive vehicles. Nissan has invested a further £3.7 billion in the site since 1984 and continued to produce new car models at the plant, including the electric Nissan LEAF.

The significance of the Nissan plant extends beyond its direct impact. The plant supports 27,000 jobs in the regional supply chain[1]. It has also contributed to upskilling the local workforce and building a strategic relationship with Japan, leading to other original equipment manufacturers such as Hitachi and Komatsu to invest in the region too. The plant has also provided a platform on which emerging strengths in related industries such as batteries and energy storage are being built.

The North East’s other longstanding specialism is in pharmaceutical and chemicals manufacturing. Chemical manufacturing has been a significant presence in the wider North East since the development of the Imperial Chemicals Industries plant in Billingham 1920s. The business base in the sector has become more diverse and fragmented over time, but the sector still contributes significantly to employment, skills, and exports through a cluster of pharmaceuticals businesses in the North East LEP area.

These longstanding strengths have been joined by a growing specialisation in offshore, wind power manufacturing and subsea technologies. This can be seen as an example of an industry pivoting, first from shipbuilding to the offshore oil and gas boom of the 1970s and 80s, and now to offshore renewables. The approval of several large wind farms off the coast of the North East region, including Dogger Bank, has further stimulated the growth of an offshore energy industry. The existence of these regional specialisms provides a strong business base on which North East manufacturing can expand in the future.

Using data from the UK business counts the North East LEP found that in 2022 there were 3,975 enterprises in the advanced manufacturing area across the North East LEP. Advanced manufacturing also employed 67,000 people in 2021. In common with most areas of the economy, most enterprises in advanced manufacturing were SME’s (less than 250 employees) with these enterprise accounting for 99% of the total. However, advanced manufacturing also accounts for an above average proportion of the North East LEP’s large enterprises. Advanced manufacturing accounted for 7% of all enterprises in the North East LEP area but 15% of large (250+ employees) enterprises in 2022.

In 2021, the subsector with the largest number of employments was research, development, and engineering, accounting for 16,000 employments and 24% of the total employment in advanced manufacturing. The next largest sectors were metals (including machining) and motor vehicles manufacturing. These three subsectors accounted for 60% of employments within advanced manufacturing.

The sectors with the highest proportions of large firms were motor vehicles production, chemicals production and pharmaceutical and medical production (8%, 7% and 5% respectively).

Data information: Data is for the North East LEP area by each of seven Local Authorities within the LEP's boundaries. Enterprises are defined as the smallest combination of legal units (generally based on VAT and/or PAYE records) that has a certain degree of autonomy within an enterprise group. Enterprises in the advanced manufacturing area have been defined using 5 digit SIC codes selected by the North East LEP.

Data information: Data is for the North East LEP area. Enterprises are defined as the smallest combination of legal units (generally based on VAT and/or PAYE records) that has a certain degree of autonomy within an enterprise group. Enterprises in the advanced manufacturing area have been defined using 5 digit SIC codes selected by the North East LEP.

In common with most areas of the economy, most enterprises in advanced manufacturing were SME’s (less than 250 employees). These enterprises accounted for 99% of the total business population. However, advanced manufacturing also accounts for an above average proportion of the North East LEP’s large enterprises. Advanced manufacturing accounted for 8% of all enterprises in the North East LEP area but 15% of large (250+ employees) enterprises in 2021.

Data information: Data is for the North East LEP area by each of seven Local Authorities within the LEP's boundaries. Employments includes employees plus the number of working owners. The BRES therefore includes self-employed workers as long as they are registered for VAT or Pay-As-You-Earn (PAYE) schemes. Self employed people not registered for these, along with HM Forces and Government Supported trainees, are excluded. Employments in the advanced manufacturing area have been defined using 5 digit SIC codes selected by the North East LEP. Subsector totals may not sum correctly due to rounding.

In 2020, the subsector with the largest number of employments was metals (including machining), accounting for 14,000 employments and 22% of the North East LEP total. A further 12,000 were employed in motor vehicles manufacturing (19%) and 10,000 in research, development and engineering (16%). These three subsectors accounted for 56% of employments within advanced manufacturing.

Data information: Data is for the North East LEP area. Employments includes employees plus the number of working owners. The BRES therefore includes self-employed workers as long as they are registered for VAT or Pay-As-You-Earn (PAYE) schemes. Self employed people not registered for these, along with HM Forces and Government Supported trainees, are excluded. Employments in the advanced manufacturing area have been defined using 5 digit SIC codes selected by the North East LEP. Subsector totals may not sum correctly due to rounding.

Data information: Data is for the North East LEP area. Employments includes employees plus the number of working owners. The BRES therefore includes self-employed workers as long as they are registered for VAT or Pay-As-You-Earn (PAYE) schemes. Self employed people not registered for these, along with HM Forces and Government Supported trainees, are excluded. Employments in the advanced manufacturing area have been defined using 5 digit SIC codes selected by the North East LEP.

The 2008 recession had a significant impact on the UK’s economy and led to significant long-term consequences. The North East LEP in particular has seen relatively slow levels of real GDP growth since the recession, with the economy only growing at 1.3% per year from 2009 compared to 1.6% for England excluding London. After taking into account the effects of population and inflation in the North East LEP’s economy was larger in 2006 than it was in 2014.

Manufacturing was hit especially hard in 2008, with sector output falling by 8% between 2008 and 2009 in the North East, compared to a 3% fall for the whole economy . Manufacturing output also recovered much more slowly than the rest of the economy. The North East’s overall output had returned to 2007 levels by 2012. Manufacturing did not reach these levels again until three years later in 2015. In contrast the services sector in the North East was already at 2007 levels by 2011.

Economic shocks such as 2008 can having a scarring effect on the sector, as skilled workers may be forced to leave the sector taking their experience with them. In the North East there is some evidence that advanced manufacturing was less severely impacted by the 2008 recession. Motor vehicles manufacturing in the North East for instance was only below 2007 levels of output for two years in 2011 and 2012, while chemical production was only below 2007 levels for one year in 2011.This highlights the importance of advanced manufacturing to regional resilience in the face of economic shocks.

Real GDP per head, North East LEP and England excluding London (1998-2020)

Source: Regional economic activity by gross domestic product (ONS, last updated 24 Apr 2024, next update April 2025) Data information: Annual estimates of economic activity by UK country, region and local area using GDP (gross domestic product). GDP estimates are workplace-based, allocated to the area in which the economic activity takes place.

"Real GDP" per head is published as the GDP "chained volume measures (CVM) per head". Changes in this measure are not impacted by inflation or changes in population, unlike changes in total GDP. Geography: North East LEP area, England, England excluding London

The North East LEP in particular has seen relatively slow levels of real GDP growth since the recession, with the economy only growing at 0.5% from 2009 compared to 1.3% for England excluding London. After taking into account the effects of population and inflation in the North East LEP’s economy was larger in 2006 than it was in 2019.

Manufacturing was hit especially hard in 2008, with sector output falling by 10% between Q1 2008 and Q3 2009, compared to a 6% fall for the whole economy . Manufacturing output also recovered much more slowly than the rest of the economy. The UK’s overall output had returned to Q1 2007 levels by Q2 2011. Manufacturing did not reach these levels again until three years later in Q2 2014. Prior to the onset of the COVID-19 pandemic in Q4 2019 manufacturing output was still only 9% higher than in Q1 2007 while total UK output was 19% higher.

The national and regional economy is currently in the processes of recovering from the unprecedented shock of the COVID-19 pandemic. The onset of the pandemic led to falls in business activity, consumer spending and employment on a scale that has rarely been seen in modern times. By Q4 2020 regional output in the North East was 6.0% below the level seen in Q4 2019[1]. The disruption to employment, skills and supply chains is also likely to have significant downstream effects on the regional economy in the future.

Manufacturing in the North East region was not as severely affected by the initial economic shock as some other sectors. Manufacturing output in Q4 2020 was 3.1% below its level in Q4 2019. This was below the North East region total (+6%) but a significantly smaller decrease than some other sectors such as Education (-16%) and Accommodation and food services (-34%)[1].

The ‘second round’ effects of the pandemic however, still had a significant impact on the sector. At the end of the furlough scheme in September 2021 9% of eligible employments in manufacturing were on furlough in the North East region. This was the third highest of all sectors[2]. The automotive subsector also experienced significant disruption due to a shortage of semi-conductors essential to car production. As a result, the number of cars built in UK factories fell by 27% year-on-year to 37,200 in August[3]. This shortage also had a clear impact on road vehicles exports from the North East which fell from £808 million in Q1 2021 to £401 million in Q2 2021. In Q1 2022 road vehicles exports were still only 82% of 2014 levels (slightly higher than the West Midlands which on 72%), while exports of other commodities from the North East had returned to 2014 levels.

Skills shortages (particularly in logistics), global material shortages and increases in the costs of shipping are likely to lead to increased shortages in the future.[4]Moreover, as was demonstrated by the arrival of Omicron and subsequent ‘Plan B’ measures at the end of 2021, the end of the COVID-19 pandemic is likely to be unpredictable rather than a smooth easing of public health measures and return to pre-pandemic norms.

a, bOur Economy: Insights into the impact of COVID-19 and the EU transition on the North East economy (2021)

One of the other significant changes to the broader economic environment has been the UK’s exit from the European Union. The UK formally exited the union on the 31st of January 2020 entering a transition period until the 31st December 2020. On the 1st of January 2021 the UK ceased to be a member of the EU single market and Customs Union, having agreed the UK/EU and EAEC: Trade and Cooperation Agreement in December 2020.

The UK’s exit from the European Union has led to changes to the procedures and regulations underpinning the import and export of goods to the EU. Border controls were introduced in stages to allow businesses the time to adapt. Full customs checks were applied in January 2022.

The UK’s exit from the European Union also ended the free movement of workers between the UK and EU. The UK provided the opportunity for EU citizens to apply to the EU settlement scheme, which allowed EU, EAA and Swiss citizens resident in the UK prior to the 31st December 2020 with the opportunity to receive settled or pre-settled status (and therefore remain in the UK). 5,589,000 individuals had been granted settled or pre-settled status by the end of September 2021, including 45,600 in the North East LEP area[1].

Despite the EU settlement scheme the foreign-born population of the UK appears to have fallen significantly since 2019. In Q3 2020, the estimated foreign-born population of the UK was 8.3 million, down from 9.2 million in the same quarter a year earlier[2]. This was a decline of 894,000 or 10%. The foreign-born population of the North East also fell from 5.6% to 4.5%[2]. The change in the migrant share of the population for the UK appears for both EU and non-EU born groups, with the labour force survey suggesting a 0.9 percentage point decline in the non-EU born population share and a 0.5 percentage point decline for EU citizens[2]. There is a considerable degree of uncertainty surrounding these figures due to changes away from face-to-face data collection due to COVID-19 and the likely overestimate of the UK’s current population. However, anecdotally the trend of reduced numbers of foreign nationals is in accordance with staffing shortages in many sectors.

Wider manufacturing, including advanced manufacturing, is one of the sectors most dependent on foreign workers in the North East. In June 2021 4% of payrolled employments in manufacturing in the North East were EU nationals, the highest proportion of any sector apart from accommodation and food services. A further 2% of payrolled employments were non-EU foreign nationals.

The number of EU nationals in North East manufacturing continued to grow between 2014 and 2019, increasing from 3,500 in July 2014 to 4,600 in July 2019. However, the overall totals have declined since 2019, falling to 4,300 by June 2021. Non-EU nationals employed in North East manufacturing increased from 1,500 in July 2014 to 2,100 in June 2021.

EU nationals working in UK manufacturing possess different qualifications to the UK national workforce. While EU nationals working in manufacturing overall are slightly less likely to possess a degree level qualification than UK nationals, 50% of those from the EU 14 possess such a qualification. These highly skilled workers are crucial for UK manufacturing and EU-Exit has led to uncertainty about their continued residence in the UK.[3]

^Home Office, EU Settlement Scheme statistics (2021)

a, b, cThe Migration Observatory, where did all the migrants go? Migration data during the pandemic (2021)

^Annual population survey, three-year aggregate data, respondents who selected manufacturing as primary industry of employment (Jan 18-Dec2020)

North East exports by EU and Non-EU markets over time

In the short run EU-Exit provided a significant positive stimulus to UK manufacturing. Manufacturing output increased 3% between Q4 2018 and Q1 2019, the largest % increase in GVA since 1999[1]. This is generally thought to be in response to stockpiling of goods prior to the UK’s exit.[2] The longer-term impact economic impact of EU-Exit has been more difficult to measure because of the concurrent onset of the COVID-19 pandemic. However, qualitative research undertaken for the North East LEP’s report on the impact of COVID-19 and EU-Exit identified a series of challenges and opportunities for businesses in the region[3]. This includes businesses in the wider manufacturing sector.

Other manufacturing (including automotive manufacturing) was identified as one of the sectors that relied heavily on trading with the EU, with many firms in the sector experiencing additional costs and delays while transitioning to the new administrative systems. The impact, however, has varied widely by firm. Large firms that had the resources to adapt to the new regime have adjusted to the new system and are now operating largely as normal. Smaller firms have experienced much greater disruption, and many have ceased trading with the EU.

Overall 28% of North East firms in all sectors said that they had faced additional transportation costs due to the end of the EU transition period in April 2022, while 22% said they had faced extra costs due to red tape. 43% said they faced no extra costs[4].

Some manufacturing firms have been using EU-Exit as an opportunity to re-shore activity in the UK, potentially leading to greater employment opportunities in the region. MAKE UK feedback suggests that up to a quarter of manufacturing businesses intend to re-shore activity back to the UK to address weaknesses in their global supply chains, as well as to increase production and protect jobs and skills domestically. Many firms in the manufacturing sector have also identified opportunities in markets beyond the EU because of EU-Exit. Firms have suggested there may be opportunities to grow exports to Australia, Asia-Pacific and South America. It is worth noting however, that the Office for Budget Responsibility’s long-term projections for UK exports suggests that UK exports will be 15% lower in the long run than if the UK had remained in the EU. They also suggest new trade agreements will have little significant impact due to the UK already having substantial agreements with non-EU partners under the EU’s existing trade agreements.[5]

The consequences of EU-Exit are still to be fully realised due to many subsections of the EU-UK free trade agreement still being subject to final confirmation[6]. One of the most significant of these is the Northern Ireland protocol. Currently the protocol avoids the need for a customs border on the island of Ireland by leaving Northern Ireland within the EU’s customs territory and single market for goods, but consequently this requires a customs border within the Irish sea which has proven disruptive to internal UK trade[7]. The UK wishes to renegotiate the current assumption that goods entering Northern Ireland are EU bound unless this can be proven otherwise and remove the European Court of Justice from the protocol, which could lead to the UK triggering the protocol’s safeguard clause[7]. These future negotiations could lead to EU trade through Northern Ireland being further disrupted.

Other areas outstanding could have a particular impact on advanced manufacturing. For instance, the UK has retained for itself the right to diverge from REACH, the EU legislation on the regulation of chemicals in the EU[8]. Currently the UK has copied the existing legislation meaning the respective regulatory systems are closely aligned, but any future divergence could lead to additional costs for UK based manufactures, particularly as chemical supply chains are complex and often cross the UK-EU border several times.

In addition, while the UK/EU free trade agreement allows for tariff free trade of goods between the UK and the EU, this is subject to rules of origin requirements[9]. These requirements mean that a certain percentage of the value of the goods traded must be from either the UK or the EU. Most UK goods meet these requirements but some currently rely heavily on imports from beyond Europe. The batteries in electric vehicles for instance are typically imported from Asia. While currently the existing agreements contain a special provision for electric vehicles which allows a lower required portion of the value to be from the UK/EU this is set to revert to the higher standard in the next few years. If the UK is unable to manufacture a greater portion of these batteries in the UK this could lead to a tariff of up to 10% being applied to electric vehicles exports, which as production increasingly moves to electric vehicles could have a significant impact on the overall cost for UK manufacturers.

^Our Economy: Insights into the impact of COVID-19 and the EU transition on the North East economy (2021)

^ONS, business insights and impact on the UK economy, April (2022)

^Office for budget responsibility, Brexit analysis (2021)

^UK in a changing Europe, Manufacturing after Brexit (2022)

a, bCentre for European Reform, EU-UK Relations: there is no steady state (2021)

^House of Commons library, End of Brexit transition: chemical regulation (2021)

^UK in a changing Europe, Manufacturing after Brexit (2022)

Energy crisis and inflation

As the global economy has emerged from the COVID-19 pandemic energy prices have increased dramatically, both in the UK and elsewhere. This has been driven by a series of factors, including a longer than expected winter over 2021 which reduced reserves, the relative underperformance of renewable and nuclear based energy sources over the last year, and increased demand for gas in Asia and South America as these areas transition away from coal[1]. In the UK this has been exacerbated by the fact natural gas demand has outstripped domestic production for almost all of the last 20 years. At the same time, there’s been a consistent scaling back of storage facilities. Most comparable countries measure reserves in terms of months’ demand, while the UK has just weeks of supply[2].

Manufacturers tend to use more energy than firms in the service sector and the impact of this increase on energy prices on businesses has been considerable[3]. In the short term most firms are unable to reduce their energy usage and so must either absorb the cost or pass the cost on to consumers[3].

From a wider economic perspective, the increase in energy prices has also been the primary driver behind increased consumer price inflation in the UK and elsewhere[3]. The Consumer Price Index reached 10.1% in September, which has a range of implications in terms of how businesses need to cost their inputs and align their prices.

In their May 2022 Monetary Policy Report the Bank of England stated that they expect inflation to continue to rise over the near term reaching a peak of around 10% in Q4 2022[3]. The expectation is that consumer price inflation will fall back to 2.1% in two years’ time.

However, despite the anticipated decline of inflation back towards the 2% target, inflation has considerably worsened the overall economic predictions of the Bank of England. Businesses may also face pressures on wages in response to inflation, further increasing production costs, while consumers may reduce spending in response to rising prices. The UK’s economy is therefore now expected to contract in Q4 2022 and experience very modest growth over the next two-three years[3].

^The eco experts, The 6 key reasons behind the UK’s Gas Price increases (2022)

^Francus, L., Loeser, R. and Watson, D. Gas Explosion: What Caused the 2021 UK Energy Crisis? (2021)

a, b, c, d, eBank of England, May monetary policy report (2022)

Data information : The CPI is a measure of consumer price inflation produced to international standards and in line with European regulations. The CPI is the inflation measure used in the government’s target for inflation and compares prices this month with the same month one year ago.

CPIH (Consumer Prices Index including owner occupiers’ housing costs) is the most comprehensive measure of inflation. It extends the Consumer Prices Index (CPI) to include a measure of the costs associated with owning, maintaining and living in one’s own home, known as owner occupiers’ housing costs (OOH), along with Council Tax. Both are significant expenses for many households and are not included in the CPI.

Data information: The Bank Rate is the single most important interest rate in the UK. It determines the interest rate that the Bank of England pays to commercial banks that hold money with the Bank of England, and therefore influences the rates those banks charge people to borrow money or pay on their savings.

The Monetary Policy Committee (MPC) sets the Bank Rate and they do so in order to meet their target of 2% inflation in the UK.

The global economic situation has been adversely impacted by the illegal Russian invasion of Ukraine on February 24th 2022. This is expected to curtail international trade with Russia and Ukraine, further increase energy prices and the price of some other commodity groups, and disrupt global supply chains[1].

Trade with Russia and Ukraine has already significantly reduced due to disturbance within the conflict zone and the imposition of sanctions on Russia[2]. This may not have a large impact on the overall trade totals for the North East as both Russia and Ukraine are relatively small markets from a North East perspective. Only 2.5% of North East imports and 1.8% of exports were to these markets in 2021. However, there are particular commodity groups where the North East currnetly sources a high proportion of its imports from these markets. 25% of the petroleum, petroleum products & related materials imported into the North East in 2021 were from Russia while 46% of North East Iron and Steel imports were from Ukraine. The disruption to Iron and Steel has already impacted on the expected revenue of the Port of Sunderland through which much of this steel is imported. The overall trade totals may not be significantly impacted but the supply chains for some commodity groups may have to be altered.

The most significant economic impacts resulting from the invasion however, are likely to be the global impact on prices and the broader disruption to supply chains. Energy prices, which were already rising before the conflict, are expected to further increase due to Russia’s role as a major energy producer responsbile for 17% of the world’s natural gas supply and 12% of its oil[3]. UK gas futures rose 24% in the week following the Russian invasion (370% up over the year)[4].

The UK is less dependent than many other European countries on Russia for its energy supply importing around 13% of its total fuel (oil, gas, LNG, and electricity) from Russia in 2019. Germany, for example, imported around 30% of its total fuel from Russia in the same year[3]. However, it should be noted that UK and European energy prices tend to move in tandem, so lower imports from Russia alone may not mean that energy prices in the UK are less impacted than those in other European countries[3]. It should also be noted that manufactureres are highly dependent on European markets that import a significant amount of energy from Russia. This includes Germany, which was the North East’s single largest export market in 2021.

In terms of broader price increases Russia and Ukraine are responsible for the production of a significant share of world supply of several key commodities. From an advanced manufacturing perspective Russia contributes a large share of global supply of key rare metals, including 41% of global Palladium supply, 9% of Nickel supply, 6% of Aluminium supply and 4% of Copper. Palladium in particular is essential for the production of catalytic converters in cars and there is already evidence of the price of these metals increasing. This may further add to price pressures facing manufacturing firms in the North East.

Beyond price increase the conflict appears to be disrupting global supply chains. While modern supply chains increase security due to flexibility and many firms have proven adaptable in response to the COVID-19 pandemic, if the production of certain goods is affected this can lead to bottlenecks that have effects beyond what might be expected from direct trade links alone[2]. European measures of supply chain disruption have been increasing since the invasion of Ukraine.

The future economic impact of the Russian invasion is highly dependent on how the conflict evolves. There is also no clear timeline for how the conflcit may end, with some analysts predicting this could take years. Until the conflict does end there may be increased economic disruption in other areas.

^Institute for government, Russia-Ukraine war: how could it affect the UK economy? (2022)

a, bBank of England, May monetary policy report (2022)

a, b, cInstitute for government, Russia-Ukraine war: how could it affect the UK economy? (2022)

^CBI, The economic impact of war in Ukraine (2022)

Indices of global supply chain disruption (2017-2022)

Last updated {{:: '2022-06-09T11:56:45.000+01:00' | date: 'dd/MM/yyyy' }}

Manufacturing has changed considerably in recent years, both in the North East and elsewhere. This section explores the trends that have been changing manufacturing and how they may impact the North East LEP area.

When the UK entered the industrial revolution in the 1800s it essentially had a monopoly on large scale manufacturing. Since then, the UK has steadily faced greater competition from other nations as they also industrialised. This process has continued with the spread of globalisation as developing nations gradually advance through the value chain. The UK no longer faces competition only from other developed nations and therefore needs to actively seek a competitive advantage.

This international competition can be seen in the UK’s share of world manufacturing output. Despite the UK’s output being 96% of 1997 levels in 2020, the UK’s share of world output had more than halved from 3.9% to 1.7%.

The development and improvement of digital and related technologies is expected to change manufacturing production significantly. In particular, the potential of big data, artificial intelligence, and the ability to link products and machines through the internet of things presents an opportunity for firms redesign their entire manufacturing process. Such a redesign will allow manufacturing to become more responsive and personalised. Digitalisation could also potentially shift manufacturing towards a circular economy where outputs can be reused and inputs are more sustainable[1].

There are significant opportunities available to firms and economies that embrace digitalisation. One report from KPMG and the Society of Motor Manufacturers and Traders found that the automotive sector could potentially gain £6.9bn every year between 2017-2035 by fully embracing digitisation, while the cumulative total benefit to the economy could be £74bn by 2035[2].

In 2019 the North East LEP published a science and innovation audit identifying the ways which the North East can prepare for the integration of digital technologies in advanced manufacturing. The audit found that the North East has a strong range of regional assets in both digital and manufacturing[3]. It also highlighted there are some good examples of networks working to integrate digital and manufacturing technologies (such as the Northern Accelerator). However, the audit highlighted awareness of digital technologies, skills and training, facilities and networks and business support as key gaps in the existing regional ecosystem[4]. Overcoming these gaps will be crucial in ensuring the North East capitalises on the opportunities presented by digitalisation.

The Made Smarter review in 2017 has also highlighted that uptake of digital technologies is generally poor among SMEs[5]. As most manufacturing firms in the North East LEP area are SME’s, improving digital take-up among these firms will be important for increasing regional productivity.

^The Future of Manufacturing: A new era of opportunity and challenge for the UK Project Report (2013)

^The Digitalisation of the UK Automotive Industry (2017)

^Applied digital technologies in North East advanced manufacturing (2019)

^Applied digital technologies in North East advanced manufacturing (2019)

Related to digitalisation, technological advances in robotics and additive manufacturing (3D printing) mean there are also increased opportunities for manufacturing frims to take advantage of automation. Such automation is likely to render many routine operations in manufacturing obsolete. Benefits of successful automation can include lower production and assembly costs, better product quality, and increased resource and energy efficiency. It can also allow the UK to compete effectively in an increasingly competitive global environment despite having higher labour costs than many developing nations.

The UK has been relatively slow to adopt robotics in manufacturing compared to some other developed countries. In 2020, there were 101 industrial robots used per 10,000 manufacturing employees in the UK[1]. This was a significant increase from 71 in 2015, but the UK was still far behind its major European competitors in its industrial robot density (including Germany, France and Italy). The UK also only installed 2,205 new units in 2020, ten times less than Germany (22,302 units), about four times less than Italy (8,525 units) and less than half the number installed in France (5,368 units)[2]. This is partially due to a greater proportion of UK manufacturing being focussed on food and drink, but it may also mean UK manufacturing is missing opportunities to invest in robotics capabilities.

More recently cobots have become a feature of manufacturing in addition to tradition industrial robots. Traditional industrial robots are designed to complete a specific pre-defined task within a physical workspace. Cobots in contrast are designed to physically interact and collaborate, safely, with humans in a shared workspace. Such robots can substantially increase productivity. According to the market research report Collaborative Robots Market, the cobot market is expected to be worth $4.28 billion by 2023, growing at a CAGR of 56.94% between 2017 and 2023[3]. Due to lower costs these newer cobots are often more attractive to SME’s than industrial robots, which is significant as most manufacturing enterprise in the North East LEP are SME’s.

^Essentra components, Industry 4.0: Rise of the cobots? (2020)

The introduction of these new digital and automotive capabilities is changing the skill profile required for manufacturing employees. A recent study by KPMG on the preparedness of the UK manufacturing industry to respond to the opportunities associated with digitisation and automation found that increasing the skill level of the workforce was the number one priority in terms of boosting productivity[1]. Their findings highlighted an increasing gap between the number of STEM qualifications required and those existing in the workforce. Fully embracing the opportunities available within the advanced manufacturing sector will required a suitably skilled workforce.

Forecasts from the UK Commission for Employment and Skills in 2016 predicted that the manufacturing sector in the North East would require 19,200 new staff over the period between 2014 and 2024[2]. The vast majority of these are highly skilled roles, with the need for 2,800 managers, directors, and senior officials, 3,300 professionals and 3,100 in associate professional and technical roles. 13,000 of these roles were predicted to require at least an undergraduate degree, while the number of roles for those with no qualifications was to decrease by 2,900 from 8,100 in 2014.

The results from the North East LEP’s health and life sciences (including pharma) skills survey in December 2020 also highlighted that digital and technical skills were likely to become more important for the sector over the next 5 to 10 years[3].

^Rethink manufacturing: Designing a UK industrial strategy for the age of Industry 4.0 (2017)

^UK Commission for Employment and Skills, Working Futures, (2016)

The manufacturing workforce in the UK is significantly older than the population average. In the North East, many of those recruited into the automotive industry in the 1980s (when the Nissan Plant in Sunderland first opened) are now reaching the end of their careers[1]. The UK Commission for Employment and Skills predicted in 2016 that 35,300 workers will have left the North East manufacturing workforce over the period between 2014 and 2024 (due to retirements and leaving the sector)[2]. There is a need to replace these highly skilled workers, but fewer young adults are entering the sector than previously. There is potentially a risk of a concentration of retirements in the sector leaving the industry with an abrupt skills shortage, especially as manufacturing tends to have a slightly lower retirement age than the overall UK workforce.

These problems are compounded by the ageing of the UK’s workforce, which combined with a trend of young adults spending more time in education means there are generally few younger workers available. Recent falls in net-migration and the UK’s exit from the European Union may also mean that there is less opportunity to recruit from abroad. Recruitment challenges are one of the driving forces behind a move towards greater use of robots and automation.

^Workforce Development - Advanced Manufacturing (2019)

^Applied digital technologies in North East advanced manufacturing (2019)

In response to greater competition from abroad manufacturing firms are increasingly integrating their product and service offerings, a business model referred to as servitisation. For example, 39% of UK manufacturers with more than 100 employees derived value from services related to their products in 2011, compared with 24% in 2007[1]. A recent survey of UK manufactures by PWC also found that 78% of respondents were developing (or have developed) a servitised business model that adds value to customer relationships[2].

These servitised business models can potentially provide manufactures with a more stable financial footing in an increasingly competitive international environment, as they allow manufactures to derive value from higher aspects of the value chain. For instance, Deloitte has estimated that profits on new machine sales are generally much lower than those from after service sales[3]. Rolls-Royce, a pioneer of this approach, derived 50% of its revenue from services in 2020, highlighting how a successful servitisation model can broaden a firm’s revenue base[4].

A risk to manufacturers from servitisation is that as the balance shifts from physical products to services and software running on those products, so the lifecycle of physical products is extended. In non-servitised products there is a strong incentive to create built in obsolescence to generate future demand, coupled with designs that limit repairability. Conversely, deep servitisation necessarily requires long-lived, repairable products, with value created through services[5]. This could dampen the overall demand in terms of production units, but it may also allow for higher selling prices and a market for future product upgrades.

Effective servitisation often requires a strong degree of digitisation and automation to adapt to customer demands in an agile fashion, reinforcing the trend of increased digitisation and automation described above.

^Future of manufacturing: a new era of opportunity and challenge for the UK - summary report (2013)

^Langley, D.J. (2022). Digital Product-Service Systems: The Role of Data in the Transition to Servitisation Business Models. Sustainability, 14(3), p.1303.

Manufacturing is responsible for many high growth firms in the UK, which is significant as high growth firms are associated with higher levels of innovation and are responsible for half of total employment growth[1]. Data from the scale-up institute shows that manufacturing was the second most common sector amongst high growth firms in the North East region, and despite recent decreases the overall number of high growth firms in UK manufacturing increased between 2018 and 2019[2].

There is also reason to believe that there is latent growth potential in the sector due to the convergence of future market trends. The North East LEP recently commissioned a future markets foresight report that examined the interaction between markets trends and regional strengths to identify 17 markets with considerable potential for regional growth. The finalised list these includes many markets related to advanced manufacturing, including electric and autonomous vehicles, energy generation and storage, robotics and satellites, and bio pharmaceuticals.

These opportunities are reflected in the attitudes of UK based manufactures. Make UK recently found that at over half of UK based manufactures intend to grow their businesses by at least 20% in the next five years, demonstrating there is significant appetite for growth within the sector[3].

^Make UK, Manufacturing: State of Industry, the Potential for Growth (2022)

Emerging policy areas

Net Zero

Net Zero is a key part of the UK government’s agenda having brought forward legislation in 2019 committing to Net Zero by 2050. In 2021 the UK also held the presidency to the 26th Conference of the Parties (COP26) in Glasgow and released its Net Zero strategy ‘Build Back Greener’. This latter document outlines how the Government intends to fulfil its commitment to reaching Net Zero.

This will have a significant impact on the manufacturing sector. According to the latest data, manufacturing and construction is the third most polluting industry in the UK, responsible for 18% of UK Greenhouse gas emissions in 2020[1]. While total emissions from the industry have reduced over the last five years, this means the industry still needs to adapt significantly to reach Net Zero.

The national drive to Net Zero will also have a significant impact on demand for manufacturing products. For instance, as part of the Net Zero strategy the Government has committed to ending the sale of new petrol and diesel cars by 2030, as well as committing to ensuring all cars must be fully zero emissions capable by 2035. This has large implications for the existing automotive industry, one of the largest employers in both the manufacturing sector and in the North East LEP.

Adapting to Net Zero will also bring opportunities to the sector. MAKE UK has identified the drive to Net Zero as an opportunity to develop and manufacture new products and services, including but not limited to electric vehicles and batteries, wind turbines and hydrogen infrastructure and related products[1]. A key challenge for the industry will be to take advantage of these emerging areas whilst also adapting manufacturing process such that they are compatible with Net Zero targets.

The North East region is in a strong position relative to its regional comparators in the drive to Net Zero, although there is still considerable further progress required. Excluding externalities CO2 emissions from the North East LEP have already more than halved between 2005 and 2020. Over the same period emissions from industry have fallen by 79%[2].

Sources: UK local authority and regional greenhouse gas emissions (BEIS) (latest update: 30 Jun 2022, next update: summer 2023)

Mid-year population estimates (latest update: 25 Jun 2021, next update: Nov 2022) Data information: Local authority level statistics. Rates are expressed as tonnes of CO2 equivalent per resident.

Totals include LULUCF (Land use, land use change and forestry) and waste management CO2 emissions data.

Source: UK local authority and regional greenhouse gas emissions (BEIS) (latest update: 30 Jun 2022, next update: summer 2023) North East LEP analysis Data information: North East LEP area statistics calculated from local authority level information.

Excludes LULUCF (land use, land use change and forestry) and waste management CO2 emissions data.

Source: UK local authority and regional greenhouse gas emissions (BEIS) (latest update: 30 Jun 2022, next update: summer 2023) North East LEP analysis Data information: North East LEP area statistics calculated from local authority level information. Includes LULUCF (land use, land use change and forestry) and waste management CO2 emissions data.

One of the Government’s other flagship policy areas is the Levelling Up agenda. This agenda aims to ensure that everyone in the UK has the opportunity to flourish by ending the extensive geographic inequality between different local areas. The objective of Levelling Up policy is to increase productivity, employment, pay, and living standards by growing the private sector, especially in areas that are currently underperforming.

The Government’s ambitions were set out in the February 2022 Levelling Up White Paper[1], which outlines 12 Levelling Up missions intended to provide clarity and consistency on policy objectives across government, with measurable outcomes by 2030. These missions cover a wide range of areas, including living standards, innovation, skills, and pride in place. Alongside each of these missions the Government published a series of provisional metrics against which progress on each mission is to be monitored. These metrics, particularly the metrics for mission 1 (living standards) provide a framework for understanding how growth in the advanced manufacturing sector can contribute to the Levelling Up agenda.

Advanced manufacturing already makes a key contribution to many of these metrics within the North East, particularly productivity, employment, and regional exports. In terms of productivity, productivity per hour worked in Sunderland is £38 per hour, significantly above the £33 per hour average for England excluding London[2]. This is largely due to the highly productive automotive cluster in Sunderland and further growth in the sector could help bring overall productivity per hour in the North East LEP closer to the England excluding London average. The sector is also already well positioned to grow due to its embrace of the transition to electric vehicles, with the global electric vehicle market alone predicted to grow at a CAGR 22.6% between 21-25[3].

In addition to productivity, advanced manufacturing also makes a key contribution to regional employment, with 67,000 individuals in employment in the sector across the North East LEP in 2021[4]. Not only this, but these employment opportunities are located in some of the more deprived areas of the North East LEP, and therefore contribute towards employment where the overall labour market is relatively weak. For example, the major employer in the sector, Nissan, is located in Sunderland, which of the 316 local authorities in England (excluding the Isles of Scilly) is the 23rd most income-deprived[5]. Future growth in the sector, building on an existing skills base and ecosystem, can potentially further increase employment in relatively deprived parts of the country. The 21 sites across the North East Enterprise Zone, which enterprises in advanced manufacturing can benefit from, further help ensure that employment opportunities are distributed across the North East LEP area.

These employment opportunities are not limited to the sector itself, for as outlined in the North East Strategic Economic Plan growth in areas of strategic importance also contributes to employment in supporting sectors. In the case of manufacturing there are particular links to growth in employment in logistics through increased exports. Not only does this further increase the contribution of the sector towards regional employment, but growth in exports disproportionally impacts deprived and disadvantaged neighbourhoods, as the wards adjacent to the region’s ports are amongst the most disadvantaged in the region. As manufactured products tend to be exported through ports, these wards are more likely to benefit from growth in the sector.

In addition to its contribution to productivity and employment the sector is responsible for the majority of regional goods exports and a significant proportion of regional service exports. Machinery and transport equipment was responsible for 45% of North East exports in 2021, chemical and related products 24% and manufactured goods classified chiefly by material a further 16%. Road vehicles exports alone accounted for 21% of North East exports in the same year, while manufacturing service exports were the second largest industry grouping in 2019 accounting for 21% of the North East total. Growing the total value of regional exports can build on this already strong sectoral contribution.

Another key objective of Levelling Up policy is to improve pride in place, with Mission 9 focused on residents’ perception of their local area. Manufacturing has a long and distinguished history across the North East, which is reflected in positive public attitudes towards the sector and related industries. The growth and development of the sector can build on this heritage and contribute to regional pride.

In the Levelling Up White Paper, the government commits to supporting private sector partnerships and clusters to catalyse economic growth, job creation, and innovation. The North East Automotive Alliance (NEAA) and the North East of England Process Industries Cluster (NEPIC) are identified in the White Paper as examples of successful private sector initiatives.

The COVID-19 pandemic has illustrated the advantages of possessing significant domestic manufacturing capability whilst also exposing the risks associated with relying on external markets for key products. For instance, during the early stages of the pandemic, the Ventilator Challenge UK consortium was established to accelerate the production of medical ventilators[1]. This consortium consisted of significant UK industrial, technology and engineering businesses from across the aerospace, automotive and medical sectors. Approximately 14,000 devices were produced in around three months, accounting for over a half of all the ventilators available to the NHS frontline in July 2020[2]. The shifting of production at pace to critical products is indicative of the strength of the UK manufacturing sector and the strategic benefits this strength can provide.

At the same time demand for medical products and personal protective equipment exceed supply during the pandemic, while sectors across manufacturing experienced supply chain disruption. The British Generic Manufactures association for instance has highlighted that approximately 20-25% of UK generic medicines are manufactured in the UK, 40-45% in the EU, and 30-35% in India[3]. While this global supply chain held up relatively well during the pandemic the margins were tight. The Generic Manufactures Association has called for a strategic approach to ensuring the future supply of generic medicines, particularly for products deemed high risk in the event of a future pandemic.

Beyond COVID-19 there is also a growing awareness of the instability of some key trade routes. For instance, in March 2021 the Ever Given container ship was grounded within the Suez canal for six days. This led to 369 ships in a tailback waiting to pass through the 193km canal on either side of the blockage, and it was estimated that the closure of the Suez canal could cost global trade between $6bn to $10bn a week and reduce annual trade growth by 0.2 to 0.4 percentage points[1]. There are also concerns that the risk of piracy, already costing the world economy $12 billion a year, may have become more acute due to COVID-19[2].

While support for reshoring is not universal across the manufacturing sector a significant minority of manufacturing firms intend to re-shore at least some of their production. 37% of surveyed manufacturing firms in 2019 claimed to be planning to move previously offshored processes back to the UK[3]. MAKE UK also found that up to quarter of manufacturing firms intend to re-shore manufacturing capability[4].

^Our Economy: Insights into the impact of COVID-19 and the EU transition on the North East economy (2021)

Internationalisation

A further element of the UK government’s policy agenda is to increase the value of the UK’s exports. Made in the UK, Sold to the World was released in November 2021 and is a refresh of the UK’s previous 2018 trade strategy[1]. The ambition of the strategy is to reach £1 trillion exports annually before the current projections which suggest that milestone will be reached in the mid-2030s. It notes that exports are key to driving increased capacity in sectors crucial to the success of the Net Zero strategy.

The new trade strategy also focuses on increasing exports in strategic sectors to maximise the UK’s competitive advantage. This includes sectors in which the UK is already a world leader, such as clean economy, and sectors of national significance, such as shipbuilding.

The strategy is to be supported through a 12-point plan for action. A key aspect of this plan includes the opening of new markets to UK exports through new trade deals, with the ambition to have these cover 80% of UK trade by the end of 2022. This includes trade deals that have been reached in principle with Australia and New Zealand and the ambition to ascend to the CPTPP, one of the largest free trade areas in the world covering Asia pacific and the Americas. The Government also announced the beginning of free trade negotiations with India in January 2022 with an aim to conclude an agreement by the end of the year[2]. These future agreements are focussed on the Asia-Pacific region as the Government believes future world growth will be driven by markets in this area.

The wider North East region has a significant opportunity to capitalise on this strategy. The North East already has a high exports per head compared to the rest of England. Specific aspects of government policy are also likely to create opportunities for the North East region. This includes the creation of the Tee’s valley free port, officially opened in October 2021. This low-tax customs zone is expected to provide a £3.2billion boost to the local economy over the next five years[3]. The Government has also opened a second DIT headquarters in Darlington, providing close proximity to the DIT for regional exporters. The opportunities provided by this infrastructure on the North East’s LEP’s doorstep have the potential to significantly increase the exporting capability of the North East LEP’s advanced manufacturing sector.

The North East LEP is also actively working with partners across the region to increase North East exports, having published a new trade and exports strategy in June 2021. This strategy highlighted opportunities to build on existing high levels of exports, the trend of increasing global service exports and the growing digital transformation of manufacturing. Advanced manufacturing, offshore energy and subsea technologies and healthcare and pharmaceuticals were also all highlighted as sectors with existing and future exports potential.

As highlighted in the Levelling Up section above, this future potential builds on the already strong contribution of manufacturing to North East exports. In 2021 the North East exported goods worth £12 billion, including £2.4 billion of Road Vehicles exports. The North East also exported manufacturing services worth £1.4 billion in 2020, with exports from the sector increasing even despite a decline in overall exports totals from the North East.

^Department for International Trade – Made in the UK, sold to the world (2021)

^DIT, UK launches India negotiations to kick off 5-star year of trade (2022)

^ITV, Open for business: Teesside Freeport is officially in operation (2021)

North East service exports by industry, £Millions, (2020)

Underpinning the Government’s ambitions with respect to building back better, Net Zero and internationalisation is their innovation strategy. This strategy highlights successful innovation in the private sector is an essential part of the UK’s future prosperity and therefore essential to achieving the UK’s other objectives. The innovation strategy was released in July 2021 and states that the Government’s objective is to make the UK a global hub for innovation by 2035[1]. To achieve this the strategy outlines a series of key actions, grouped into four pillars, unleashing businesses, people, institutions & places, and missions & technologies.

The innovation strategy commits to not just designing innovative products in the UK but also manufacturing them domestically. This can reduce the delay between innovation and product launch, realising the gains from innovation more rapidly. It also ensures the resilience of key sectors such as health and life sciences in accordance with the reshoring agenda outlined above. The development of advanced manufacturing is therefore key to underpinning successful innovation.

Advanced manufacturing in the North East possesses considerable regional assets that can accelerate innovation and contribute to the wider innovation agenda. For example, the North East is home to the Centre for Process Innovation (CPI). The CPI helps companies develop and scale-new innovative products by providing access to valuable expertise and networks, and currently has over 550 staff and five sites across the North East of England.

The automotive & advanced practice group (AMAP) hosted by the University of Sunderland is another important regional innovation asset. Offering business support to advanced manufactures across the region, AMAP aims to inform, inspire, and innovate in advanced manufacturing through the application of research and knowledge. They are also responsible for hosting the Sustainable Advanced Manufacturing project, a £10.9m project to support product and processes development within the SME manufacturing base in the North East funded by the European Union Regional Development Fund.

Despite these regional assets however, there are also structural challenges facing the region that limit the potential for regional innovation. One of the most significant of these is the low level of research and development spending per head in the North East, which is lower than all other English regions. In addition, the strength of alternative centres of research and development such as the West Midlands means that even firms in sectors where the North East is a national leader perform their R&D outside the region.

Overall, the significant regional innovation assets in the North East, along with the further assets outlined in the next section, mean that advanced manufacturing in the North East is well positioned to contribute the Government’s goal of making the UK a global hub for innovation by 2035. One of the Levelling Up missions commits to increasing public R&D spending outside the Greater South East by at least 40% by 2030. This increased expenditure will be key in unlocking regional innovation.

Sources: Business enterprise research and development, UK (ONS; last updated 19 Nov 2021), Mid-Year Population estimates (ONS via Nomis; last updated Jun 2021) Data information: Based on UK nations and regions. The North East region includes the North East and Tees Valley LEP areas.

Existing regional asset base

Infrastructure

The North East LEP benefits from containing several ports, including the Port of Blyth, the Port of Tyne and the Port of Sunderland. The LEP area also has easy access to the new free port in the Tees Valley. Together these ports provide convenient access to global markets for North East based firms and in 2020 alone 19 million tonnes of goods were exported out through these ports[1].

The advanced manufacturing sector in the North East LEP is further able to take advantage of the 21 sites across the North East Enterprise Zone. These sites provide either business rates discounts or enhanced capital allowances which can allow firms in the North East LEP to gain a competitive advantage. The sites were strategically selected to build on existing strengths across the North East LEP’s economy, including the existing advanced manufacturing business base. They are also dispersed widely across the North East LEP areas allowing businesses across the whole region to benefit from the available opportunities.

International Advanced Manufacturing Park – One of the 21 sites in the North East Enterprise Zone, the first phase of developing the International Advanced Manufacturing Park concluded in November 2020. Major manufacturing companies such as SNOP UK, Faltec and Envision AESC have already committed to the site, while phase two of the development is due to add a further 221,997 sq m floor space. The park aims to have created 7,000 new jobs by 2030

The A19 Corridor – Also one of 21 sites in the North East Enterprise Zone, this was the UK's first designated area for Ultra Low Carbon Vehicles. Near to the UK home of Nissan and a global automotive supply chain, this site has a focus on low carbon vehicles and advanced manufacturing^Sunderland Echo (2021)

Beyond the port connections the North East LEP also benefits from a substantial logistics and public transport infrastructure. In 2020 alone 47 million tonnes of goods were lifted by road freight from the North East region[1]. The North East also benefits from the Tyne and Wear metro, one of the most extensive light rail systems outside of London which supported 33 million passenger journeys in 2019/2020[2]. This logistical and transport capacity ensures that goods can be delivered to market and the employees can access employment opportunities across the North East.

Located in the neighbouring Tees Valley, many firms operating in the North East LEP will be able to benefit from the infrastructure and industrial cluster centred on the Teesworks industrial zone. This 4,500-acre site is at the heart of the Tees Valley free port and is the UK’s largest industrial zone.

Enabling sectors

The North East LEP is home to four universities, Newcastle, Northumberland, Sunderland, and Durham. These universities are a critical source of skills for the region, including the advanced manufacturing sector. In 2019/2020 5,990 students enrolled in engineering and technology degrees in the North East LEP. The universities also play a critical role in conducting and organising relevant research efforts. Newcastle university has a particular strength in engineering technology research, while Sunderland university is responsible for managing the Sustainable Advanced Manufacturing Project.

There are nine further education colleges in the North East LEP area, providing critical technical education and further learning opportunities. These colleges are brought together through the North East LEP College Hub which brokers strategic employer partnerships with further education institutions. In 2020/21 1,650 students started Engineering and Manufacturing Technologies apprenticeships in the North East LEP area. Previous analysis from the North East LEP has also highlighted a strength in engineering and manufacturing technology in the region’s further education sector.

The North East LEP has a substantial financial, professional and business services sector. This includes the headquarters of established brands such Virgin Money and Newcastle Building Society, and new and innovative companies such as Atom Bank, World Pay, True Potential, Wire Card and Scott Logic. The major presence of this sector provides manufacturing firms in the region with access to financial and business support services that are key for supporting growth.The expertise of the sector can also assist manufacturingfirms embrace the growth of servicization.

The North East LEP is home to a growing digital sector, with the number of firms in the sector having grown 295 between 2015 and 2021 and reaching a total of 2,680 in 2021. The North East has existing specialisms in software, cloud computing, communications, buildings information modelling, and gaming, in addition to emerging specialisms in data analytics, immersive technologies and cybersecurity. With digitalisation set to reshape the future of advanced manufacturing the presence of an innovative digital sector in the North East is a major asset.

Construction is also a strong contributor to the North East economy, with the North East benefiting from several mid-sized construction firms. While construction sector faces its own challenges, particularly in terms of skills, the presence of these midsized construction firms provides advanced manufacturing enterprises with the opportunity to expand existing production sites.

Networks and advocacy organisations

The North East Automotive Alliance is an industry-led cluster group that supports the sustainable growth and competitiveness of the automotive sector in the North East. The largest automotive cluster group in the UK with over 300 participants, the NEAA explores topics including advanced propulsion and energy.

Advanced Manufacturing Forum is a membership network that connects manufacturers and engineers across the North East. It provides support to drive sustainable growth, innovation, best practice and collaboration amongst its members.

North East Pharma advocates on behalf of and supports North East based pharmaceuticals companies. It does so through developingand communicating information about North East pharmaceuticals, ensuring the long-term supply of skills, and developing and securing the national and global supply chain.

Bionow is a membership organisation supporting the biomedical, pharmaand life sciences sectorsacross the North of England. They provide a range of specialist business support services, including a procurement support scheme and accelerator programme designed to help businesses scale.

The North East Process Industries Cluster is a not-for-profit membership organisation supporting the chemical processing sector in the North East of England. The cluster actively engages with the entire chemicals value chain to help drive the regional economy.

Make UK are a national membership organisation aiming to create an environment in which UK manufacturing can thrive. They do this by championing issues importantto their members andoffering a range of business support and advice services. MAKE UK has a dedicated Northern Make UK membership and external affairs team.

The Engineering and Manufacturing Network offers companies across the engineering and manufacturing industries expert support and assistanceso that they can realise their full potential.

NOF is a business development organisation helping to make valuable connections between businesses in the global energy sector. They work to connect companies with the best and most innovative supply chain businesses in the UK.

Existing enterprises

The North East is home to leading OEM's including Nissan Motor Manufacturing UK, Hitachi, Komatsu, Caterpillar, Erwin Hymer Group and Cummins. These OEM’s are responsible for producing over 502,000 passenger cars and commercial vehicles, 6,400 non-highway vehicles, over 325,000 engines and 20% of all Electric Vehicle production across Europe.

The North East has an established pharmaceutical manufacturing base, including GSK, Organon, Accord Healthcare, Pharmaron, Sterling, Quotient, and Piramal Healthcare.

The North East has also developed a strong offshore energy and windpower cluster, in part due to its excellent proximity to key UK offshore wind development sites such as Dogger Bank, Firth of Forth and Hornsea. This includes many firms within the offshore renewable supply chain such as Soil Machine Dynamics (SMD), Tekmar, BEL Valves, Baker Hughes, Fabricom, and Royal IHC Limited.

Recent investments into the region by SSE and Equinor on the Tyne, and RWE at Port of Blyth to provide key bases to lead the development of the Dogger Bank windfarm continue to demonstrate the region’s opportunity to play a strategic role in development and construction roles in this sector

Innovation and business support

Centre for Process Innovation – Part of the High Value Manufacturing Catapult and headquartered in the North East, the Centre for Process Innovation (CPI) helps companies develop and scale new products and processes. This includes companies operating in the pharmaceutical, automotive and chemical sub-sectors. They have a team of over 550 scientists, engineers, and business specialists who can helping companies to develop, prove and commercialise new products and processes.

National Formulation Centre – One of the sites in the CPI, the National Formulation Centre offers tailored solutions for developing and optimising liquid and powder formulations, nanomaterials, composites, chemical processes and new technologies. The site provides state of the art facilities and skilled personal who can help local enterprises develop solutions to their product needs.

The National Printable Electronics Centre – Is a further site in the CPI that accelerates the commercialisation of printed and flexible electronics. By providing an environment where companies can test and develop concepts the centre supports innovators through the challenges of scaling products and process.

Offshore renewable energy catapult – The ORE catapult is UK’s leading technology innovation and research centre for offshore renewable energy and plays a key role in accelerating the development of UK companies in the offshore renewable energy sector. Their site at Blyth contains world leading assets for the testing of renewable energy technology.

The Robotics and Autonomous Systems Test Site – Part of the Offshore Renewable Energy Catapult this new testing site for emerging robotics technology is the first of its kind in the UK. The site was awarded £3 million from the government’s Getting Building Fund in February 2021.

Made Smarter programme – The Made Smarter programme supports businesses to get to market faster, cut costs and reduce downtime. It does so by helping businesses invest in digital tools, innovations and skills. Support through the Made Smarter programme in the North East LEP is available via the North East Growth Hub.

Automotive & advanced practice group (AMAP) – Hosted by the University of Sunderland AMAP aims to inform, inspire and innovate in advanced manufacturing through the application of research and knowledge. They offer support to local businesses by sharing contacts and best practice, providing training, and undertaking research.

Sustainable Advanced Manufacturing Project – Is a £10.9m project to support product and processes development within the SME manufacturing base in the North East. The project is a collaboration between the European Regional Development Fund and the University of Sunderland and is managed by Sunderland University through AMAP.

North East Centre of Excellence in Satellite Applications – The Centre helps businesses to exploit the use of satellite data, technology and applications to gain a competitive advantage in a global market. The Centre works with both organisations that are currently in the space sector but also those that have potential to operate in the sector but have not yet investigated the opportunities.

Innovation Supernetwork – The Innovation Supernetwork aims to help North East businesses bring innovative products and services to market. They do this by providing bespoke innovation support to small and medium sized enterprises in the North East LEP area, as well as increasing connectivity and sharing best practice.

Materials processing institute – Located in the neighbouring Tees Valley, this research and innovation centre focuses on the development of materials and commercialisation of technologies for the industrial processes

The Welding institute – Located in the neighbouring Tees Valley, the Welding Institute is a leader in materials research, covering a wide range of technologies for industrial sectors

The industrial digitalisation technology centre – Located in the neighbouring Tees Valley and led by Teesside university, the centre helps local businesses explore the opportunities available through industry 4.0 and digitalisation

Further information

Digital Technology Evidence Base

Read our evidence base covering the North East Digital Tech Sector.