From 7 May 2024, The North East Evidence Hub is a project of the North East Combined Authority. Find out more at northeast-ca.gov.uk/north-east-lep

Cloud computing

Cloud computing refers to the on-demand delivery of computing services over the internet, hosted at a central data centre and often managed by the Cloud Service Provider (CSP). This includes services across server requirements, application hosting, data storage, networking, software, and analyticals.

This is one of the 16 market profiles produced as part of the Economic Market’s foresight study commissioned by the North East LEP. It provides an overview of the future growth prospects for the Cloud Computing market globally, a summary of the enterprise base serving the market in the North East and relevant regional assets, and an analysis of how the continued convergence of global trends will affect future market development.

These markets were selected as those most likely to present opportunities for future regional growth in the North East LEP. This was done based on a trends analysis conducted by Frost and Sullivan, which identified 37 high impact trends driving continued change and growth in these markets globally. A shortlist of markets from this trends analysis was then cross-referenced against the current North East position by Cambridge Econometrics. This analysis identified the most significant opportunities for the North East LEP.

Each of these profiles also uses findings from the Data City platform to quantify the number of firms serving the Cloud Computing market in the North East. This platform links companies house data to companies’ websites and uses the website text and machine learning to classify firms into Real Time Industrial Classification Codes, which can allow analysis of markets often too emergent to be precisely measured in SIC codes. The data from this platform has been triangulated against ONS data to consider a variety of perspectives on the market.

More detail about the methodology can be found here for the 16 market profiles.

Emergent status

in the North East and associated value chain

National scope

National scope in terms of firm activities and ownership

Moderate presence

sightly more firms with locations in the North East than the national average

Description and global outlook

Cloud computing refers to the on-demand delivery of computing services over the internet, hosted at a central data centre and often managed by the Cloud Service Provider (CSP).

This includes services across server requirements, application hosting, data storage, networking, software, and analyticals. The model inherently allows the service delivery to be flexible, which can be customised to the customer’s requirements.

Market drivers

Cloud technology will have a significant positive impact on a range of operations dealing with data, application management and connected ecosystems, especially processing of data at edge sites, enabling secure and high-performance outputs.

Cloud computing has enabled faster design and development of Internet of Things (IoT) solutions, such as RF filters and MEMS12 filters, creating virtual models in 3D, helping to explore new designs quickly and avoid expensive physical prototyping.

The market for cloud computing is expected to be supported in the coming years with wider introduction of 5G services, increasing adoption of edge computing, increased demand for artifical intelligence (AI) and data analytics services, improved cybersecurity and the ever increasing number of connected IoT devices.

The major challenges facing the cloud computing market are:

Data security

Lack of skilled workforce

Multi-cloud environment

Cost management

Compliance

Time to migrate.

Scale and scope of global market

The market was estimated to be US$ 312 bn in 2020, with the growth rate predicted to be about CAGR 17% for the period 2021-2025. The US was the largest market for public cloud solution in 2019, followed by countries such as the UK, Germany, Japan and Australia.

The UK is among the leading countries for the cloud computing market, which is supported by strong internet access, data security and IPR protection. Some of the leading global companies in the cloud computing market are Google, Amazon Web services, Microsoft Azure, IBM Cloud, Alibaba Cloud, Salesforce, SAP, VMWare, and Oracle for example.

Capital flows and FDI

Funding for ICT and data ventures (VC and PE-based) rose by 183% between 2019 and 2020. This is expected to be higher in 2021, partly as a result of the COVID pandemic, but also buoyed by the increasing numbers of innovative startups and growth companies in the market across the UK. This represented 42.6% of all VC and PE investments made across the nation over the period.

$312 bin

The market was estimated to be US$ 312 billion in 2020, with the growth rate predicted to be about CAGR 17% for the period 2021-2025.

As with other markets, the regional breakdown of this capital liquidity does not favour the North East, with an aggregated 1.1% of all investments made in the North East region. There appears to be significant regional differences in either availability of private capital, or the readiness of regionalised ventures to attract such investment.

Of specific interest in cloud computing context is the FDI component, with North American and European data powerhouses being drawn to nations and regions with ready skill markets and favourable siting economics for offshoring their large datasets. In a post-brexit environment, this may be curtailed from previous expectations, but the potential remains high for FDI in this area.

North East presence and capabilities

Regional overview

The North East has established strengths in software development, programming, service centres and gaming. There is a rapidly growing North East FinTech sector and the region has MedTech, GovTech, and Connected Construction expertise; and AI / VR / Augmented Reality technical expertise. The region hosts the Sage HQ – a FTSE 100 listed company – as well as hosting offices for Accenture, Ubisoft and Atom Bank. Other major organisations include HM Revenue and Customs Digital Delivery Centre and the NHS Business Services Authority. Successful SMEs include Hedgehog Lab (app developer for Deliveroo, Clever Clinic, Pix Pac, Deliciously Ella); Zerolight (specalising in real-time 3D visualisation) and new innovative firms such as Wordnerds, So Post, Coatsink, Inflo Software, Tharsus, and Everflow Group.

R&D strengths include IC3 (the International Centre for Connected Construction); the Digital Catapult, the National Innovation Centre for Data (Newcastle Helix); and the Centre for Public Health Data. University specialisms include Computing at Durham University, Northumbria University’s BIM Academy, and the Faculty of Computer Science at the University of Sunderland. North East Satellite Applications Centre of Excellence is based in NETPark, County Durham. Delivered by Sunderland Software City, Digital Catapult North East Tees Valley (NETV) supports businesses from across the region to encourage the growth and adoption of advanced digital technologies.

Key business and industry networks include:

SunderlandSoftwareCity

Digital City, Digital Union

Dynamo

VRTGO Labs/Proto Lab

Thinking Digital

The Newcastle Tech Trust.

Key sites and assets include:

Digital Catapult North East and Tees Valley

Satellite Applications Catapult

Sunderland Software City

VRTGO Labs/Proto Lab

Cobalt Data Centre; Digital Quarter

Immersion Labs

Gateshead and Stellium Data Centres.

The North East LEP area has a strong and diverse university sector, with over 85,000 students studying at four universities: Durham University; Newcastle University; Northumbria University and University of Sunderland. In 2018/19 there were 31,475 enrolments in the four universities in the North East LEP area.

It has been a priority of the North East LEP to increase the enrolment in STEM qualifications. Overall, the change in total graduates between 2014/15 and 2018/19 and who studied a STEM related subject has been roughly in line with the UK average at around 10%. However, some subjects have experienced a much faster increase in graduates, most notably in computer science, where the number of graduates increased by over 40% in the space of four academic years, compared to 19% in the UK as a whole.

According to the North East LEP local skills report, 3.5% of employment in the area was in digital occupations, comprising 42,700 people - a smaller proportion than England as a whole (4.4%). However employment in these occupations has grown faster in the North East LEP area between 2015 and 2020 than nationally (Growth of 24% in the North East LEP area compared to 18% nationally). Notable occupations at the three digit level that grew faster than England excluding London between 2015 and 2020 were Information Technology and Telecommunications Professionals (grew by 39% in the North East compared to 19% in England excluding London) and Research and development managers (140% growth vs 27%).

Analysis of GVA and employment by SIC sectors

The table below summarises the findings from socio-economic data and economic forecasts for the IT Services industry, the most relevant SIC classification industry to cloud computing for which Cambridge Econometrics forecasts are available.

The IT Services industry employs 24,400 in the North East, with a similar share of regional employment to nationally. The sector has high productivity, and has experienced a steep increase in employment and GVA. The outlook is forecast for a further increase in jobs and GVA growth.

The Data City Findings

The Data City provides company data based on an AI-driven taxonomy search of terms and content on company websites. This is then connected to companies house data for each company – and allows an aggregate analysis for new industry and market definitions. The data captures the number of business branches in the North East LEP area.

The Data City suggests there were 65 active firms in cloud computing in June 2022, representing 2.7% of all UK firms in this sector.

Local Authority location quotients

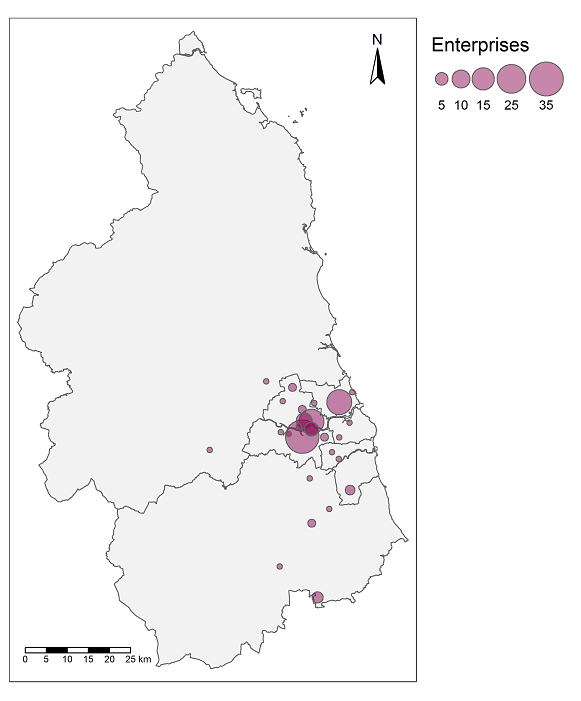

In terms of overall enterprise counts, the data suggest that Gateshead, North Tyneside and Newcastle are all centres for cloud computing services. Each of these local authorities had a very strong location quotient in the Data City results, and Gateshead in particular had a location quotient in the top 10 nationally. In contrast, the other four local authorities in the North East LEP area had location quotients below the national average.

Connections with other regions

The locations data from the Data City suggests that cloud computing firms in the North East LEP area are much more likely to have locations in more than one region. In June 2022 72% of cloud computing firms in the North East LEP had a location in at least one other NUTS region, compared to only 31% UK firms that had a location in more than one NUTS region.

This was also reflected in the specific regions in which North East LEP firms had locations. Except for the North West, North East LEP firms were more likely to have a location in other regions than UK firms overall in every region and nation. The North East LEP had very strong links to Yorkshire and the Humber, Scotland and Northern Ireland in particular.

Cloud computing and sector crossover

One of the innovative features of the Data City methodology is that it allows firms to be classified in multiple sectors. The platform does so through real time industry classifications (RTICs), which are constantly evolving classifications generated by an AI from companies’ websites. Firms can be classified under multiple RTICs at any one time.

This means the data can be used to demonstrate interdependencies where sectors overlap. In terms of the North East LEP cloud computing sector, over 10% of North East LEP firms operated in the data infrastructure, cyber and data landscape RTICs. In each case these firms were moderately more likely to operate in these sectors than firms in the UK overall, suggesting that there might be a greater degree of interdependency between these sectors in the North East LEP than nationally.

Overall, in the UK cloud computing firms operated in an additional 34 sectors, of which North East LEP cloud computing firms operated in 18.

Cloud computing and subsectors

The Data City methodology also includes individual subsectors within the RTIC taxonomy which allows detailed analysis of the North East LEP’s focus within cloud computing. These subsectors suggest that the North East LEP has a very strong focus on cyber threat management compared to nationally, as well as a strong focus on data infrastructure software, data landscape enablers, and cyber network security.

Overall, in the UK cloud computing firms operated in 116 sub RTICs, of which firms in the North East LEP operated in 37.

North East LEP Clusters

As suggested by the location quotients, cloud computing firms in the North East LEP area are concentrated in Gateshead, Newcastle and North Tyneside. There is a particular concentration near the bank of the River Tyne between Gateshead and Newcastle city centres.

Regional prospects

A critical part of this study is to shortlist which emergent markets represent “hot prospects” for the North East economy in the future. Using the findings from the study, and the assessment framework below, Cloud computing is rated as a market with:

Emergent status in the North East

National scope in terms of firm activities and ownership

Moderate presence in the North East with 2.7% of firms in this market having a location in the North East LEP (compared to 2% of firms in all markets).

As the global digital economy has developed Cloud computing infrastructure and associated capabilities around the processing, quality management, validation and structuring of large datasets has become fundamental to digital operations. This means innovative data platforms are in high-demand and this demand is expected to grow as the complexity of data produced and consumed across the nation’s digital landscape also grows.

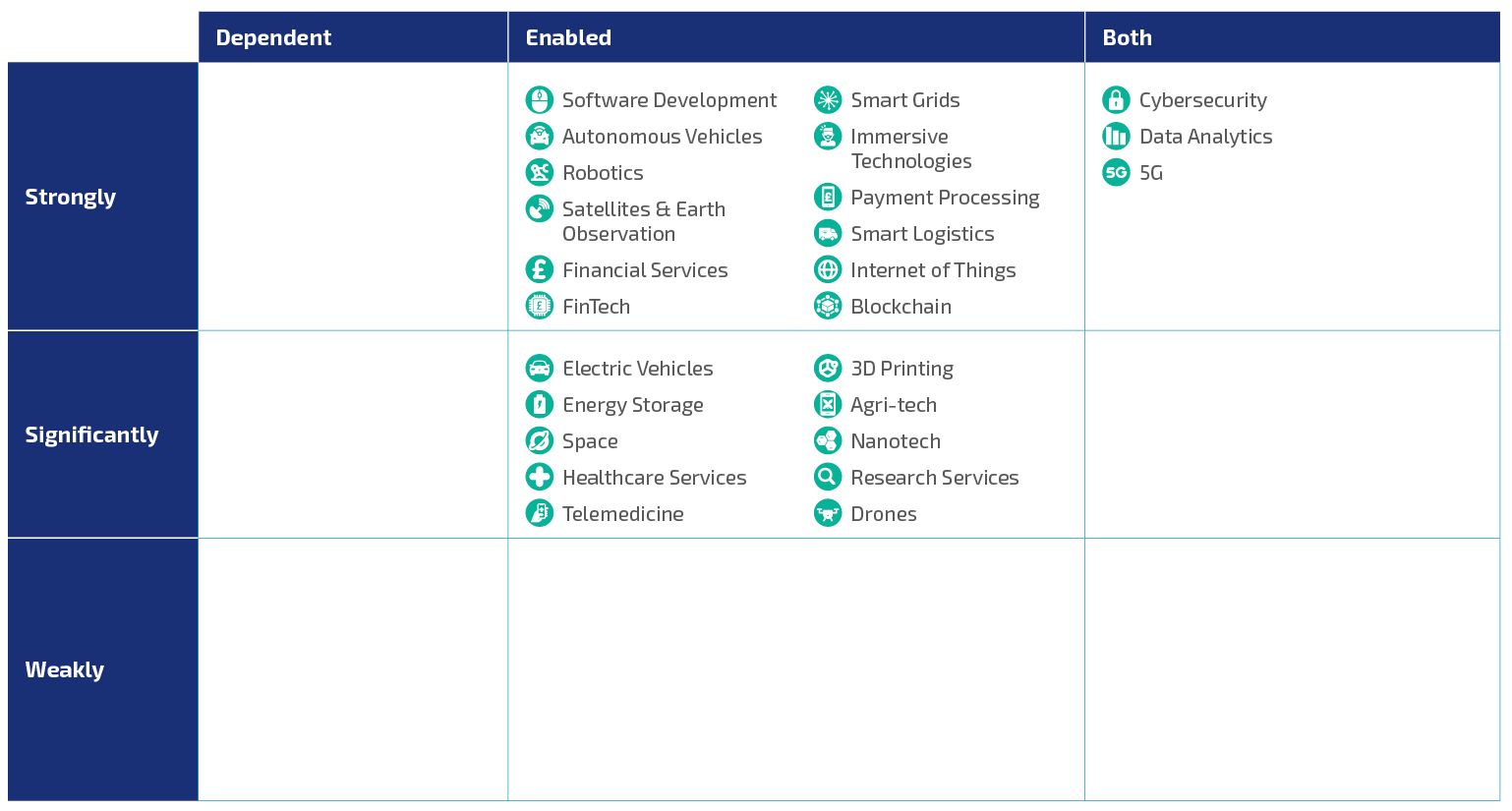

The importance of this market goes beyond the direct potential for growth too, because as is highlighted in the table below a wide range of markets are enabled by cloud computing capabilities. This includes markets where the North East is already looking to cement a competitive advantage, such as Fintech and Immersive Technologies. More broadly almost all forms of digitally enabled business models rely on cloud computing services and platforms to operate and evolve, which means cloud computing is essential for growing regional productivity.

Cloud computing is therefore both a significant opportunity and key area of competency for the North East. The region already enjoys a strong position in the race to establish regional competency centres and attract talented data scientists, architects and engineers. This is a highly competitive field however, and the North East needs to consider how to strategically differentiate itself from other regions.

Part of this differentiation can be linked to the core dependencies of this market. As highlighted in the table, Cloud computing is heavily dependent on the maturity of Cybersecurity, data resilience capabilities and next generation networks. There may be an opportunity to exploit the growth and maturing strengths that the North East has in Cyber security and telecommunications innovation to offer highly secure, resilient data centre services as a regional specialism.