From 7 May 2024, The North East Evidence Hub is a project of the North East Combined Authority. Find out more at northeast-ca.gov.uk/north-east-lep

Financial Services

Financial services refers to the broad set of services delivered to individuals or corporations across banking, investment, financing, insurance, credit facilities, fund-transfers, FinTech, InsurTech etc.

This is one of the 16 market profiles produced as part of the Economic Market’s foresight study commissioned by the North East LEP. It provides an overview of the future growth prospects for the Financial Services market globally, a summary of the enterprise base serving the market in the North East and relevant regional assets, and an analysis of how the continued convergence of global trends will affect future market development.

These markets were selected as those most likely to present opportunities for future regional growth in the North East LEP. This was done based on a trends analysis conducted by Frost and Sullivan, which identified 37 high impact trends driving continued change and growth in these markets globally. A shortlist of markets from this trends analysis was then cross-referenced against the current North East position by Cambridge Econometrics. This analysis identified the most significant opportunities for the North East LEP.

Each of these profiles also uses findings from the Data City platform to quantify the number of firms serving the Financial Services market in the North East. This platform links companies house data to companies’ websites and uses the website text and machine learning to classify firms into Real Time Industrial Classification Codes, which can allow analysis of markets often too emergent to be precisely measured in SIC codes. The data from this platform has been triangulated against ONS data to consider a variety of perspectives on the market.

More detail about the methodology can be found here for the 16 market profiles.

Established status

in the North East and associated value chain

National scope

in terms of firm activities and ownership

Moderate presence

sightly more firms with locations in the North East than the national average

Description and global outlook

Financial services refers to the broad set of services delivered to individuals or corporations across banking, investment, financing, insurance, credit facilities, fund-transfers, FinTech, InsurTech etc.

Over the past decade, financial services industry has been experiencing landscape shift in the market with advent of new business models, customer delivery platforms and processes which has enabled it to grow across new sectors.

Market drivers

Adoption of technologies such as cloud, AI, predictive analytics, blockchain, and digital platforms has been driving the growth of new business delivery models for the financial services. For example:

car commerce

crypto currency

chip-based credit cards

robo-advisors for investment services

The pandemic has also impacted financial services, with increasing focus on new delivery models and customer engagement. Digital transformation is one of the key approaches for global financial companies to adapt to changing market needs. The market across developing economies is also experiencing growth owing to the increase in smartphone penetration, internet accessibility and the low cost of digital platforms which can provide services in remote and rural areas.

The major challenges facing the financial services markets are:

high cost of digital adoption

increasing competition from start-ups

compliance challenges

emerging business models

data security

customer retention

Scale and scope of global market

The global market size for financial services market was estimated at US$ 20.5trillion in 2020, with the forecasted growth rate to be CAGR 6% for the period of 2021- 25. China and the US are the world’s largest financial services markets with considerable banking presence.

Along with UK, the top three destinations are home to some of the largest banks globally, and are supported by a large number of non-banking entities including investment firms, Non-Banking Financial Companies (NBFC), and trading houses.

Financial services are the biggest export earning market for the UK, highlighting the UK’s capabilities in the sector. The UK is among the leading destinations for financial services including insurance, and home to several global companies. The market is supported by availability of talent, a growing FinTech segment, professional services and regulatory support.

Some of the leading global financial services companies are: J.P. Morgan Chase, Visa, Mastercard, Citi Bank, Bank of America, United Health Group, Industrial and Commercial Bank of China, AXA, PayPal Holdings, HDFC Bank Limited, and BlackRock.

UK Market

From a capital perspective, most banks are in a stronger position now than before the last crisis (in 2008), with more than three times more capital. Agreements not to pay dividends and bonuses have further fortified their position, allaying fears of immediate existential risk to the UK’s major banks. Historically low interest rates and fierce competition have increasingly pinched margins for more than 10 years, and recent emergency base rate cuts from central banks will ensure margins remain compressed for the foreseeable future.

As Covid-19 heaps pressure on revenue growth and increases credit losses, navigating this near-zero rate environment will be even more difficult. Banks will therefore need to transform their cost base while still providing positive customer and employee outcomes. In the absence of opportunities to substantively improve the top line, cost reduction is the only lever available to improve financial performance. Banking is set to be transformed by digital technologies and services, new forms of lending (e.g. Fintech), and an environment of credit losses and stagnant lending growth.

The insurance industry has been hit by Covid-19 related claims from business disruption, travel disruption, ill-health and increased mortality. Furthermore, insurers’ capital strength will suffer as a result of falling asset values. Consumer demand has also changed, with a significant increase in support services for health insurance. Against a challenging backdrop of lower earnings, as well as an increase in claims, insurers will have to focus on transforming and digitising their operating models to build in flexibility, agility and new income streams.

Capital flows and FDI

Nationally, VC, PE and Buyout deals for private sector capital into financial services has fluctuated over the past 4 years. Fintech has accounted for a large proportion of the private and VC deals completed, with a larger balance of international investment into UK firms than any other market in this report.

The majority of capital flows in financial services are however expected to come from corporate group investments into regional hubs from larger banking coroporates wishing to relocate or invest in existing North East locations. These corporates are themselves funding R&D and providing extensive capital for development of Fintech IP, both internally, and with local firms and research organisations.

UK government-backed funds for R&D associated with Fintech and broader Financial Services remains an accessible option for innovative ventures.

North East presence and capabilities

There is a significant financial services sector in the North East LEP area, which includes traditional banking, building societies, as well as online banking and fintech. Payment services is one of five fintech sub-sectors are thriving in the region: payments; software; data analytics; platforms; and cybersecurity.

Many leading fintech companies are located in the North East. Global company Sage, Newcastle Strategic Solutions, Kani Payments and True Potential are all headquartered here, as well as Atom, one of the UK’s foremost neobanks, which is based in Durham. Major banks such as Virgin money, TSB, Newcastle Business Society, Tesco Bank and NS&I are based in the North East. HMRC has its digital delivery headquarters in the region and employs specialists across various technical digital fields to deliver new digital technologies to its customers.

Many leading fintech companies are located in the North East. Global company Sage, Newcastle Strategic Solutions, Kani Payments and True Potential are all headquartered here, as well as Atom, one of the UK’s foremost neobanks, which is based in Durham. Major banks such as Virgin money, TSB, Newcastle Business Society, Tesco Bank and NS&I are based in the North East. HMRC has its digital delivery headquarters in the region and employs specialists across various technical digital fields to deliver new digital technologies to its customers.

The region is also home to several enterprise software development companies that have tech teams embedded in top-tier investment banks.

Financial services companies moving to the North East have a huge choice of dedicated office accommodation and innovation hubs, including Sunderland Software City, TusPark and Salvus House all nurturing fintech, insuretech and cyber businesses.

Located in the Newcastle Helix, the national innovation centre for data helps organisations large and small generate insight from data, including organisations in the Tech sector. The centre receives funding from the North of Tyne combined authority as part of the digital growth and innovation programme.

The North East LEP area has a strong and diverse university sector, with over 85,000 students studying at four universities: Durham University; Newcastle University; Northumbria University and University of Sunderland. In 2018/19 there were 31,475 enrolments in the four universities in the North East LEP area.

It has been a priority of the North East LEP to increase the enrolment in STEM qualifications. Overall, the change in total graduates between 2014/15 and 2018/19 and who studied a STEM related subject has been roughly in line with the UK average at around 10%. However, some subjects have experienced a much faster increase in graduates, most notably in computer science, where the number of graduates increased by over 40% in the space of four academic years, compared to 19% in the UK as a whole.

According to the North East LEP local skills report, 3.5% of employment in the area was in digital occupations, comprising 42,700 people - a smaller proportion than England as a whole (4.4%). However employment in these occupations has grown faster in the North East LEP area between 2015 and 2020 than nationally (Growth of 24% in the North East LEP area compared to 18% nationally).

Notable occupations at the three digit level that grew faster than England excluding London between 2015 and 2020 were Information Technology and Telecommunications Professionals (grew by 39% in the North East compared to 19% in England excluding London) and Research and development managers (140% growth vs 27%)

FinTech North is a not-for-profit, collaborative project conceived and created through the partnership of White Label Crowdfunding and Whitecap Consulting.

The FinTech North initiative aims to

generate collaboration and knowledge share by building a FinTech community across the Northern Powerhouse

enhance reputation of the Northern Powerhouse as a FinTech region

generate tangible economic benefit for the region and the cities within it

They do this by

managing a predominantly event-based FinTech entity focused on the the Northern Powerhouse

providing a platform for sharing best practice

showcasing regional talent and facilitating connections

They also engage with key public and private sector organisations and higher education establishments in the region.

Is an industry led group with the core mission to ‘Grow the North East Tech Economy’ through collaboration, innovation, skills. They act as a voice for the region promoting it as a centre of tech development both regionally and nationally.

Analysis of GVA and employment by SIC sectors

The tables below summarise the findings from socio-economic data and economic forecasts for both of the IT Services and Financial and Insurance industries. These are the most relevant SIC classification industries to financial services that Cambridge Econometrics provide forecasts for. Both sectors are large employers in the North East, although there are no outstanding industry specialisms relative to England less London. Productivity rates are near, or at the average for England less London. Both industries have demonstrated high rates of historic growth, and are forecast to growth strongly in future years.

IT services

Finance and insurance

The Data City Findings

The Data City provides company data based on an AI-driven taxonomy search of terms and content on company websites. This is then connected to companies house data for each company and allows an aggregate analysis for new industry and market definitions.

According to the Data City there are 210 active firms operating in the financial services market in the North East LEP area, representing 3.2% of the total firms in this sector nationally.

North East LEP Clusters

Financial services firms are distributed across the North East LEP area, but with a concentration of firms in Newcastle upon Tyne in particular.

Key search terms

The following search terms were amongst the most common ones identified on North East LEP are financial services firm’s websites. Insurance, compliance and marketing were amongst these terms, which may suggest that the North East has a focus on these areas.

Financial services and sector crossover

One of the innovative features of the Data City methodology is that it allows firms to be classified in multiple sectors. The platform does so through real time industry classifications (RTICs), which are constantly evolving classifications generated by an AI from companies’ websites. Firms can be classified under multiple RTICs at any one time.

This means the data can be used to demonstrate interdependencies where sectors overlap. In terms of the North East Financial services sector there were very few cross-sector linkages identified, which may suggest there are untapped opportunities for this sectors to operate in other markets across the North East.

Regional prospects

A critical part of this study is to shortlist which emergent markets represent “hot prospects” for the North East economy in the future. Using the findings from the study, and the assessment framework below, Financial Services is rated as a market with:

Established status in the North East

National scope in terms of firm activities and ownership

Moderate presence in the North East, with 3.2% of firms in this market having a North East LEP location (compared to 2% of firms in all markets)

Financial services are a traditional strength of the UK, with the market being supported by the availability of talent, a growing FinTech segment, professional services and regulatory support. The global market for these services is only likely to grow in tandem with economic growth globally. The challenge for the North East is to develop a distinct offer in a market where other regions including London, Leeds and Manchester have core strengths.

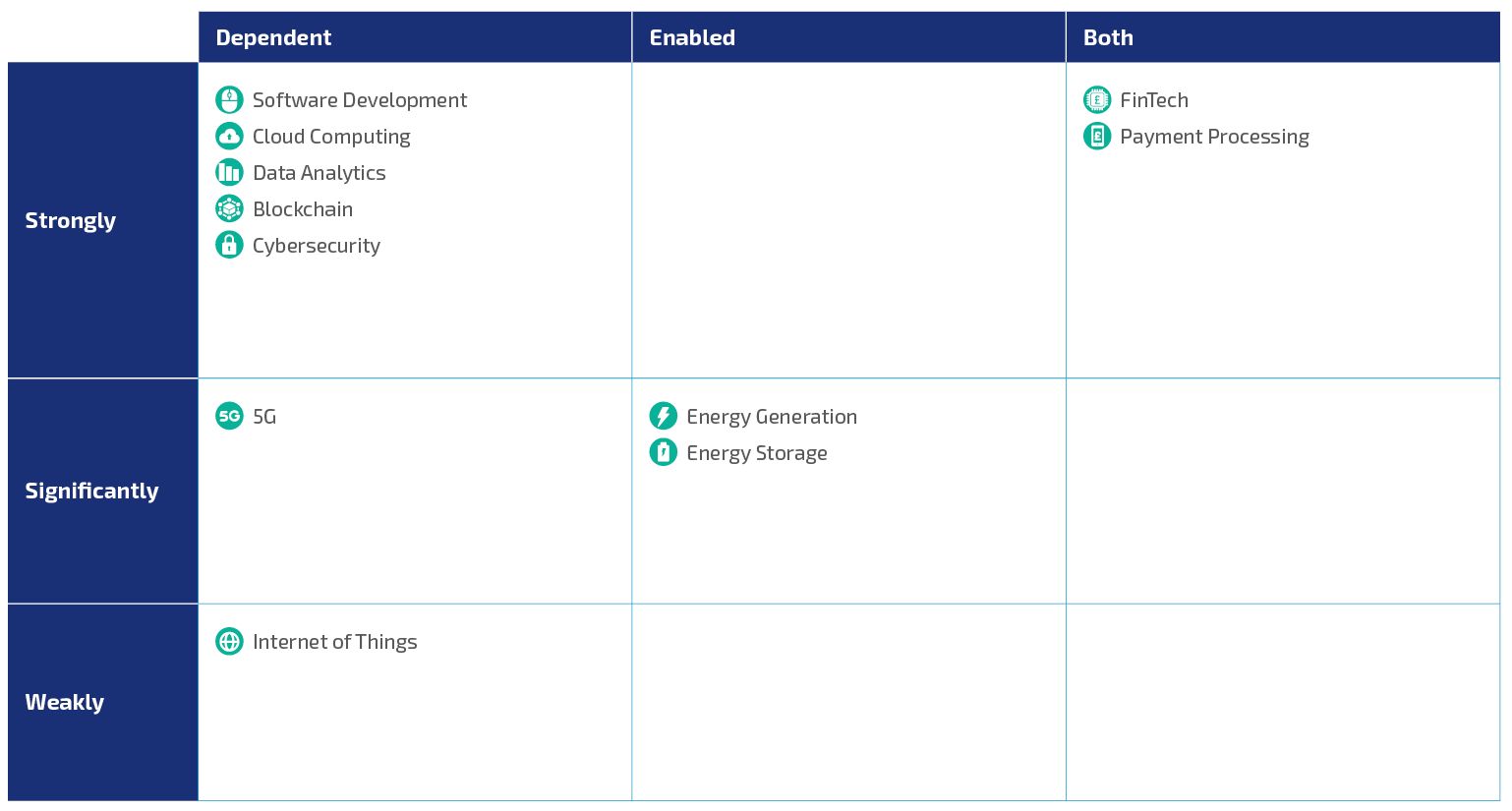

A specific opportunity exists to align Financial services with Fintech and Payment processing. As highlighted in the interaction and dependencies table these markets are both enabled by and dependent on Financial services. Several innovative cross-over business models are beginning to emerge from the interaction between the traditional financial services sector and these new digital capabilities. Both these markets are also areas where the North East has an existing area of strength, which could allow the North East to develop a competitive advantage in this market.

Additionally, the region is well-poised to take advantage of increasing demands for tailored financial instruments and products associated with the energy transition. The Green Bond market is expected to grow over the next decade. As highlighted by the dependency table Energy generation and Energy storage are both enabled by the development of Financial services, and another opportunity for North East’s Financial services sector may be to develop regional specialisms around the provision of green finance products and services.

The key dependencies for the market are the digital capabilities required to store and protect data on Financial services, especially in Software development, Cloud computing, Data analytics, Blockchain and Cybersecurity. The North East must be mindful to develop the required support capabilities if it is to develop a regional specialism in Financial services.